How to File Form 1099 for Attorney Fees and Settlement Payments in 2026

Key Takeaways (2026 Filing Season)

- $600+ payments = 1099 required. Most attorneys belong on Form 1099-NEC, while settlement gross proceeds to lawyers go on Form 1099-MISC, Box 10.

- Lawyers and law firms always get a 1099, even if they are corporations, LLCs, or LLPs, when payments for services reach $600 or more in a year.

- Missing or late Forms 1099 can trigger $60–$630+ per-form penalties and put your legal-fee deductions at risk during an IRS audit.

- The easiest way to handle Form 1099 legal fees is to integrate 1099 rules into your law firm accounting and legal accounting workflows: collect W-9s up front, track $600+ payments by matter, and use software reports for year-end 1099-NEC and 1099-MISC exports.

Complete Guide for Lawyers, Attorneys, and Law Firms

Missed a 1099 in 2025? $60 per form turns into $630K max fines when IRS audits find mismatched Form 1099 attorney payments or settlement payments.

IRS Form 1099 reports $600+ payments to non-employees, lawyers, co-counsel, or experts. Unlike W-2s for employees, these go straight to the IRS by January 31.

Lawyers and law firms: whether you’re sending 1099 for a legal wage or getting them from clients, doing this right protects your law firm’s accounting and keeps audits away.

Keep reading for simple 1099-NEC vs 1099-MISC rules, settlement tricks, and checklists that make compliance easy.

IRS Form 1099 Basics for Legal Fees

What Is IRS Form 1099 and How Is It Related to Legal Fees

IRS Form 1099 is a form for businesses regarding taxes that they send to the IRS and non-employees when they pay $600 or more in a year. Think independent contractors, freelancers, or vendors, not your regular staff who get W-2s.

For lawyers, this means a 1099 covers payments to co-counsel, expert witnesses, or outside firms. 1099 for lawyers and 1099 for attorneys kick in for things like referral fees, consulting, or case work. It’s the IRS’s way to track money flowing outside payroll.

Why Legal Fees Trigger Special 1099 Rules

Most corporations skip 1099s, but not for lawyers, even if they’re a big law firm or LLC. If you pay $600+, you must file a 1099 without any exceptions.

This matters for your law firm’s financial strategy. Clean law firm and legal accounts involve tracking these payments year-round. Miss it, and the IRS matches your deductions against the lawyer’s income report. No match? Audit flags fly.

Get this right, and your books stay audit-proof while you smoothly deduct those attorney payments on 1099.

Do Lawyers, Attorneys, and Law Firms Get 1099s?

Yes, lawyers and attorneys get a 1099 anytime a client or business pays $600+ for legal services in a year. It doesn’t matter if it’s a one-time expert witness fee or ongoing co-counsel work. The IRS wants that tracked.

Do Law Firms Get 1099s (Including Corporations)?

Law firms get 1099s from clients, insurers, or anyone paying $600+. Here’s the twist everyone googles:

Do attorneys get a 1099 if they are a corporation?

Yes, even corporations. Normal vendors (like office suppliers) skip 1099s if they’re C-corporations. But with lawyers, the IRS shows no exceptions. Is your big-firm client paying referral fees? They owe you a Form 1099 for attorney fees regardless of your LLC or corporate setup.

An S-corporation is a regular corporation that has elected special “pass‑through” tax treatment, so profits and losses are taxed only on the shareholders’ individual returns instead of at the corporate level.

When Your Firm Both Issues and Receives 1099s

Law firms live this double life. You’re issuing 1099s for law firms to outside counsel or experts. Then, clients send you Form 1099 for your work.

Match both sides perfectly in your law firm accounting transactions. Received a 1099 from an insurer? It better aligns with your income. Sending one to co-counsel? Track it as a deductible expense. Mess up the math, and audits knock.

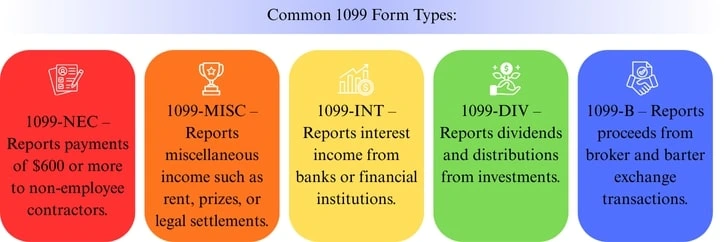

1099‑NEC vs 1099‑MISC for Legal Fees

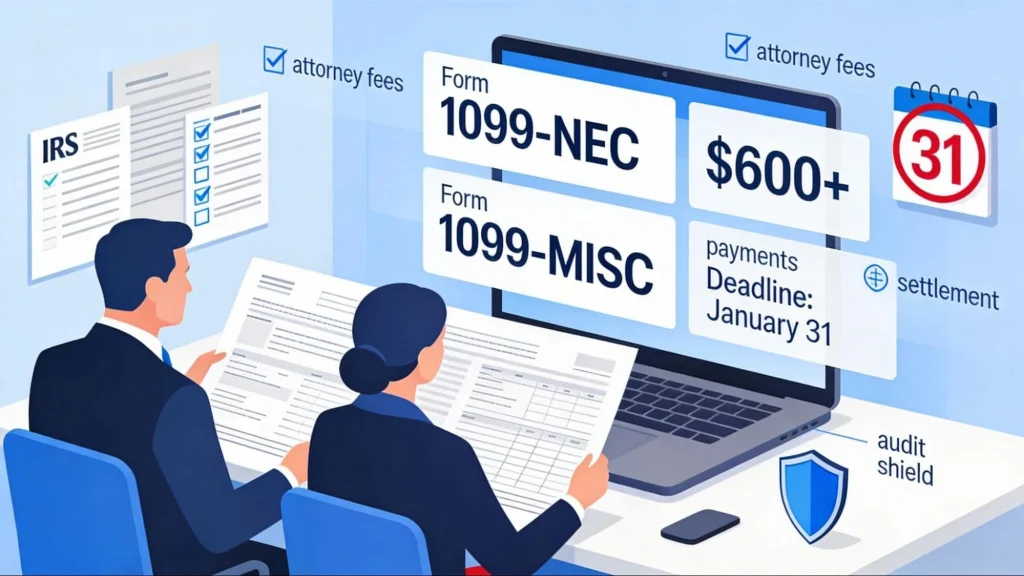

Payments to Attorneys: 1099-MISC or 1099-NEC?

Lawyers always ask: payments to attorneys 1099 misc or nec? The answer depends on what you’re paying for: services or settlement proceeds. Get this wrong, and your 1099 bounces back with IRS notices.

When to Use Form 1099-NEC for Attorney Fees

Use 1099-NEC for actual attorney fees, which covers form 1099 attorney fees and all 1099s, such as hourly work, consultations, or referral fees.

If your firm pays outside counsel $800 for case research, put it in Box 1 on 1099-NEC.

When to Use Form 1099-MISC for Legal Fees and Gross Proceeds

1099-MISC for attorney fees comes into play for legal fees, 1099-MISC, and settlements.

Here’s the key difference:

- Legal services fees → 1099-NEC

- Gross proceeds (settlement money paid to attorneys) → 1099-MISC Box 10

Insurer sends $50K settlement to opposing counsel? Report the full amount in Box 10, even if it includes their fees. Deadline: March 31, electronic.

Quick Comparison Table: 1099-NEC vs 1099-MISC for Legal Fees

| Payment Type | Who Gets Paid | Form Used | Key Box |

|---|---|---|---|

| Legal services fees | Lawyer/Law firm | 1099-NEC | Box 1 |

| Settlement gross proceeds | Attorney | 1099-MISC | Box 10 |

| Referral/consulting | Co-counsel | 1099-NEC | Box 1 |

| Client settlement share | Client (usually not) | None | N/A |

When You Must Report Legal Fees on Form 1099

Thresholds and Triggers for 1099

Pay $600 or more in a calendar year for Form 1099, and you must report it. Even if it’s cumulative, three $250 checks to the same lawyer? That’s $750 total = 1099 required.

If you pay $599? No form is needed. But if it goes over that line, the IRS expects your amount on 1099 to match the recipient’s tax return perfectly.

Common Legal Payments That Require a 1099

These everyday payments trigger 1099 for lawyers, 1099 for attorneys, and 1099 for law firms:

- Co-counsel fees for case collaboration ($1,500 over 3 months → 1099-NEC)

- Expert witness testimony ($2,000 for trial prep → 1099-NEC)

- Referral fees to other attorneys (10% of $50K settlement → 1099-NEC)

- Outside firm research or document review ($800 project → 1099-NEC)

- Settlement gross proceeds sent to opposing counsel ($25K check → 1099-MISC Box 10)

Track every dollar. Your accounting software should flag these automatically.

Payments That Do Not Require a 1099

Not everything needs a form. You can skip 1099s for:

- Your employees (they get W-2s)

- Reimbursements (lawyer’s travel, filing fees, and keep receipts separate)

- Corporations (excluding attorneys, any office supplies vendor? No 1099)

- Credit card payments (processor handles 1099-K)

- Physical injury settlements paid directly to clients (tax-free, no reporting)

Law Firm Accounting Workflow for 1099

The best way to prepare is to integrate 1099s as part of your law firm accounting, not just a once-a-year drill. Build 1099 rules into vendor setup, matter management, and payment approvals so that Form 1099 legal fees and Form 1099 attorney fees are ready to go by the time January 31 comes around.

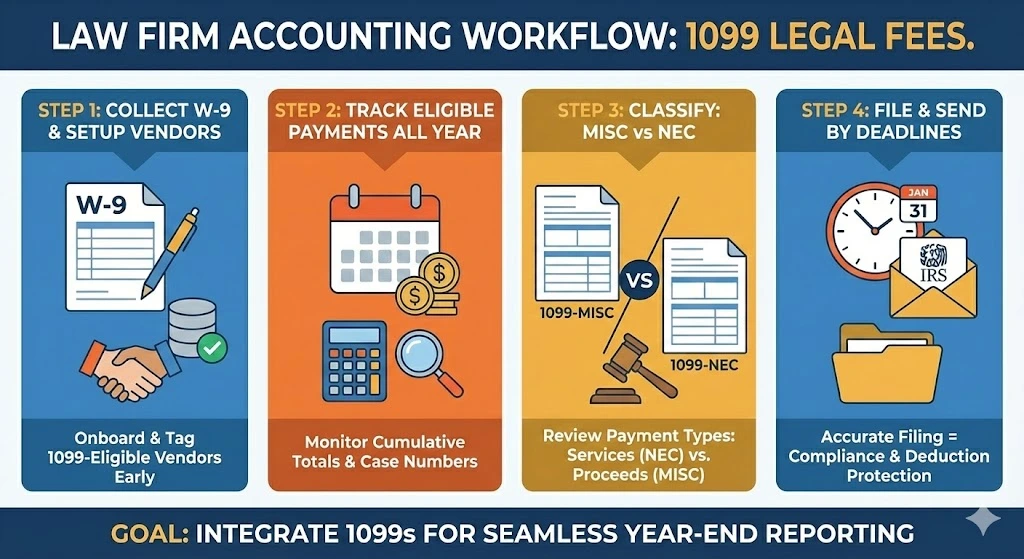

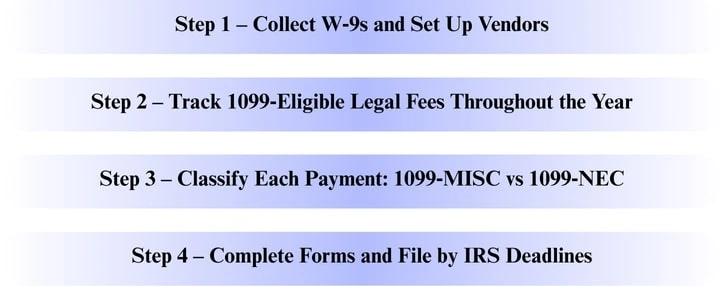

Step‑by‑Step: How to Prepare Form 1099

Step 1 – Collect W‑9s and Set Up Vendors

Before you pay any outside lawyer, expert, or contractor, collect a Form W‑9. This gives you their legal name, address, taxpayer ID, and entity type, all the details you need to decide if a 1099 applies.

Make W‑9 collection a standard part of your law firm’s financial strategy and vendor onboarding. Enter this information cleanly into your accounting or practice management system so every 1099‑eligible vendor is clearly tagged from day one.

Step 2 – Track 1099‑Eligible Throughout the Year

Next, track every payment that might later show up on a 1099. Use case numbers and vendor tags so your legal accounting shows exactly who was paid, how much, and for what work. Watch cumulative totals: three or four small payments can easily cross the $600 threshold. Good tracking now means you are not digging through invoices at year’s end.

Step 3 – Classify Each Payment: 1099‑MISC vs 1099‑NEC

When totals cross $600, decide how to report payments to attorneys 1099 MISC or NEC. As a rule of thumb, payments for legal services, like research, drafting, or court appearances, belong on a 1099‑NEC. Settlement gross proceeds paid to attorneys generally belong on 1099‑MISC, usually in Box 10. Review both the vendor’s W‑9 and what you actually paid for so each dollar lands on the right form.

Step 4 – Complete Forms and File by IRS Deadlines

Once everything is classified, you are ready to prepare Form 1099 for legal fees and Form 1099 attorney fees. Fill in the correct totals, double‑check names and taxpayer IDs, and generate copies for both the IRS and recipients.

Remember the key dates: 1099‑NEC forms usually must be sent and filed by January 31, while most 1099‑MISC filings have a slightly later IRS deadline if filed electronically. Filing early and accurately not only keeps you compliant but also keeps your firm off the audit radar and protects your deductions.

Common 1099 Legal Fees Mistakes and How to Avoid Them

Frequent 1099 Errors in Law Firm Accounting

When vendor records, W‑9s, and payments are not tracked cleanly, it becomes easy to miss required forms or send the wrong ones, which can lead to costly 1099 penalties. Building 1099 checks into your regular legal accounting, not just year‑end, keeps mistakes, penalties, and audits away.

Using the Wrong Form: 1099‑MISC vs 1099‑NEC

A classic error is using the wrong form for payments to attorneys, 1099 MISC or NEC. Service fees for legal work should not be reported as 1099 MISC. They belong on 1099‑NEC as non‑employee compensation, while settlement gross proceeds to attorneys go on 1099‑MISC (usually Box 10). Mixing these up confuses both your books and the lawyer’s tax return, and it is an easy red flag for the IRS.

Forgetting to Include Attorney Fees on 1099

Another costly mistake is simply leaving legal fees on 1099 off the radar. Small payments spread across the year can quietly pass the $600 mark, which means you now owe a Form 1099 filing. If you never issue a 1099, your deduction still shows up on your return, but the attorney’s income will not match theirs, which is exactly the kind of mismatch that can trigger a notice or audit.

Misclassifying Law Firms and Attorney Corporations

Finally, many firms assume that if a vendor is a corporation, no 1099 is needed. That works for most vendors, but not for lawyers. The question “Do attorneys get 1099 if they are a corporation?” trips up a lot of teams. The answer is yes, attorneys and 1099s for law firms are required even when they operate as C-corporations, S-corporations, LLCs, or LLPs. Treating law firms like other corporate vendors and skipping 1099s can quickly create a pattern of non‑compliance that the IRS can spot.

Building a 1099‑Ready Law Firm Financial Strategy

A 1099-ready approach should be a part of your law firm’s financial strategy, not just a last‑minute January task. When 1099 compliance is built into daily workflows, your firm protects deductions, avoids penalties, and stays prepared if the IRS ever reviews your books.

Integrating 1099 Compliance into Your Law Firm’s Financial Strategy

Treat 1099s as a core part of your law firm’s financial strategy. Capture everything early: collect W‑9s during onboarding, tag 1099‑eligible vendors, and link outside counsel, experts, and referral fees to the right matters so Form 1099s are ready to report.

Best Practices in Legal Accounting and 1099 Compliance

Strong legal accounting makes 1099s simple. Focus on:

- Clear accounts that separate legal fees, expert costs, and reimbursements.

- W‑9s are required before any payment to outside lawyers, experts, or contractors.

- Vendor and matter tags that flag payments likely to become 1099.

How Legal Software and Integrated Payments Help With 1099s

Legal software and integrated payments can automate a lot of tasks, such as

- Auto‑capture W‑9 data and mark vendors as 1099‑eligible.

- Run one‑click reports of all $600+ payments to attorneys, law firms, and experts.

- Export clean year‑end data for Form 1099 attorney fees without rebuilding spreadsheets.

This kind of setup reduces missed forms, speeds up filing, and frees your team to focus on client work instead of chasing numbers every January.

Turn 1099 Compliance Into a Core Part of Your Law Firm Accounting

At this point, you know that 1099 is more than just paperwork; it is a key piece of a strong law firm’s financial strategy. Building 1099 rules into your law firm accounting and legal accounting means clean W‑9s, accurate vendor records, and clear distinctions between 1099‑NEC attorney fees and 1099‑MISC settlement proceeds. When those pieces are in place, audits are less scary and cash flow planning is more reliable.

Use this guide as a checklist:

- Review how you collect W‑9s

- Track $600+ payments

- Choose between 1099‑MISC and 1099‑NEC

- Reconcile the 1099s you issue with the ones your firm receives

If gaps show up, consider tightening your internal workflows or using legal‑specific software that automates 1099 tracking and exports.

A short audit of your 1099 process now can save penalties, notices, and long email threads with your accountant later.

FAQs on 1099 for Legal Fees, Lawyers, and Law Firms

Yes. Lawyers get a 1099 when a business or client pays them $600 or more in a year for services. This usually goes on Form 1099‑NEC as non‑employee compensation, even if the lawyer is part of a firm.

Yes. The normal corporate exception does not apply to lawyers. Attorneys get a 1099 even if they are a corporation, LLC, or LLP when they are paid $600+ in legal fees during the year.

Yes. Law firms get 1099 forms from clients, insurance companies, and other payers when they receive $600+ for legal services or settlement‑related payments. Firms should reconcile these 1099s with their own income records.

Use Form 1099‑NEC for most attorney fees, hourly work, flat fees, referral fees, or expert work by a lawyer. Use Form 1099‑MISC (Box 10) when you report gross proceeds paid to attorneys from settlements, not the service fees themselves.

In your law firm, track all payments to outside lawyers and experts by vendor and matter. When totals reach $600+, report the service portion as legal fees on 1099‑NEC, and any settlement gross proceeds to attorneys on 1099‑MISC Box 10. Keep W‑9s, payment records, and 1099 copies together so your legal accounting matches what the IRS sees.